What really strikes me at the moment is that many countries are facing the same problem, the skyrocketing inflation, but that the reactions of the central banks are very different.

Google Translated from Dutch to English. Here is the link to the original article in Dutch. The article was originally published on 11 April 2022.

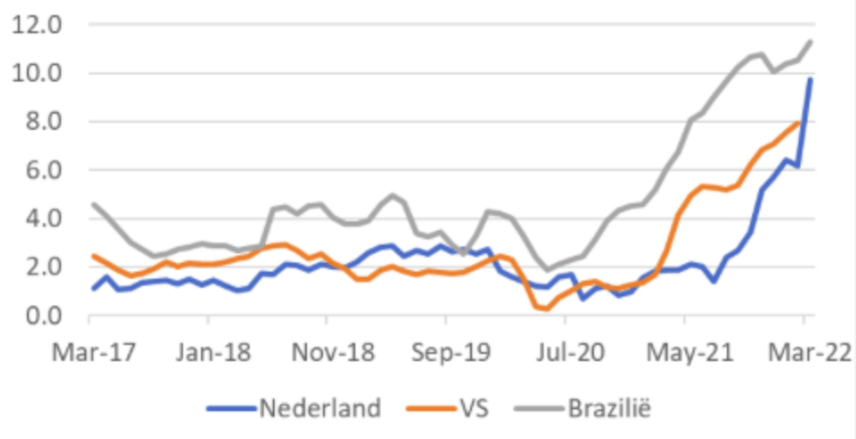

Netherlands - USA - Brazil | Inflation (%)

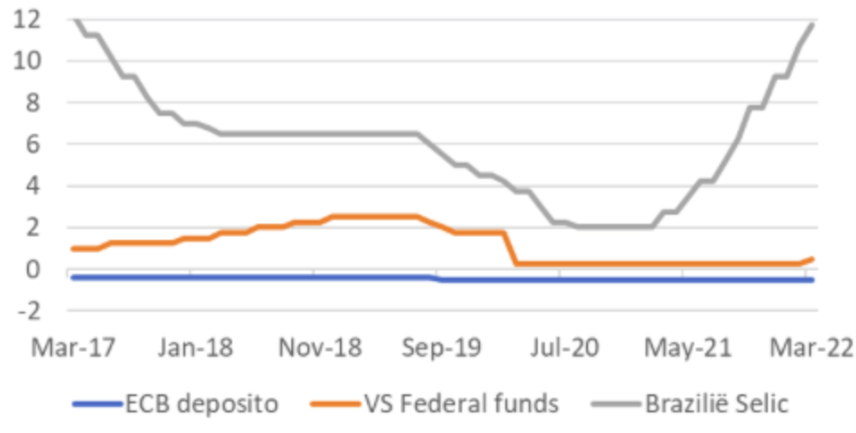

When inflation started to pick up in the course of 2020, Brazil's central bank was the first to take a look, but it sprang into action early in 2021. In total, the Brazilian central bank has already raised interest rates nine times.

The Fed has long maintained that high inflation was temporary, but has taken a spectacular turn in recent months. After the first rate hike in March, a whole series of moves have been made and the steps are likely to be larger than those in March. The Fed will also continue to shorten its own balance sheet.

The ECB, on the other hand, lacks any urgency. The deposit rate is even still negative and the bank still buys bonds.

Official Interest Rates (%)

The House of Representatives follows refresher courses on inflation

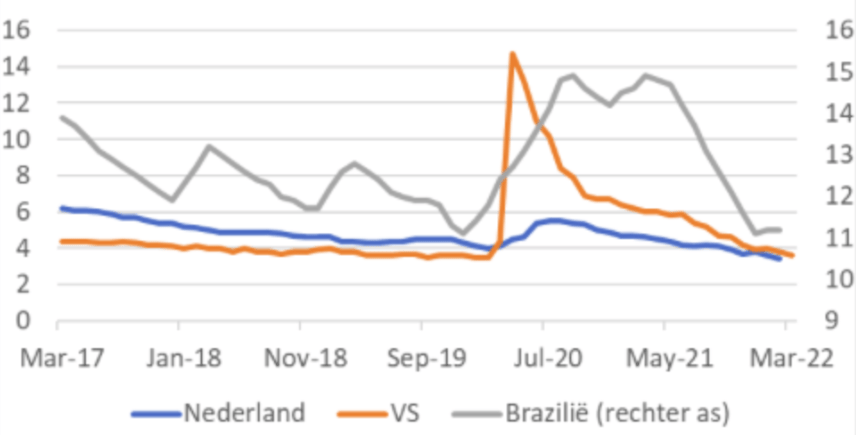

Of course, one economy is not like the other. For example, Brazil is benefiting from the rise in raw material prices, which is annoying for us. But if I look at the situation in these three economies, and then look at unemployment for example, I see insufficient justification for the divergent monetary policies.

One of the three central banks mentioned must be making a big mistake. There are two options. The first is that Brazil's central bank is tightening unnecessarily, causing damage to its own economy, and the Fed will follow suit. The other possibility is that the ECB grossly underestimates inflation risks. I suspect the latter. After all, the central bank of Brazil knows a thing or two about inflation. By contrast, we, including the ECB, are completely out of inflation. Knowledge about this has flowed away from us. Last week a kind of refresher course on this subject was even organised for members of the House of Representatives.

Netherlands - USA - Brazil | Unemployment (%)

I haven't checked, but I strongly suspect that none of the current ECB board members has ever decided on a series of rate hikes. After all, the last time our central bank started such a series was at the end of 2005!

ECB Deposit Rate (Jan. '99 - today)

Yet it is coming. When bond purchases have stopped, later this year, we can finally expect rate hikes in the eurozone as well, Christine Lagarde more or less promised.

How would an interest rate hike feel for ECB executives? It can't help but feel like they're having sex for the first time. After all, the current board members have never done it. That must be a lot of excitement for a central banker. But also uncertainty, like “am I doing it right” and those with empathy will wonder what it's like for the other person.

The graph above shows that the ECB also raised interest rates in 2008 and 2011, but those were 'mistakes' that were quickly undone. Perhaps comparable to the fidgeting of very young 'wannabe lovers' that ultimately, and fortunately, did not lead to the sex act.

Many economists also rant about inflation

It may be arrogant, but if I listen to some fellow economists, I conclude that our profession too has become so used to inflation that a great deal of nonsense is being preached. Think about it: inflation is at its highest point in living memory and unemployment at its lowest level in a long time. Apparently some colleagues think that this situation calls for the very lowest interest rates in human history. The faculty where this is taught must be closed immediately.

I also know that inflation is mainly caused by the sharp rise in energy prices and by logistical disruptions. The ECB cannot do anything about that. However, this does not alter the fact that there is an imbalance between supply and demand in the economy that monetary policy can do something about. Monetary tightening can dampen demand and bring it closer to supply before a broader and lengthy inflation process develops. Monetary policy can also ensure that inflation expectations remain anchored. You don't have to wait for the anchor to drop.

When the title of this column somehow came to mind, I immediately thought of 1978. I went on vacation in the US with my best friends, Jan and Erik. We put a homemade bumper sticker on our rental car with the text “We Dutch are better lovers”, a heroic statement for which we could not provide any proof. 44 years later I can say that this marketing strategy was spectacularly unsuccessful. When Lagarde argues that the ECB is closely monitoring inflation and will do everything it can to bring it under control, it sounds to me as plausible as the text of our bumper sticker.