- CPB presents 'call for action'

- Cabinet has financial scope for purchasing power support

- Dutch GDP growth outpaces growth elsewhere…

- …but that must be a red herring

- The US economy is now sending very confusing signals

Google Translated from Dutch to English. Here is the link to the original article in Dutch. The article was originally published on 19 August 2022

According to the CPB, the loss of purchasing power will amount to 6.8% this year. That is quite something, although the CPB predicts some recovery in purchasing power for next year: +0.6%. I heard on the radio today that everyone is shocked by that 6.8%. Where the heck have those people been these past few months? If inflation is 10% and the wage increase is 3-4%, you really don't have to be Einstein to understand that there is a significant loss of purchasing power, even though the cabinet has taken some support measures. And do not forget that the reduction of excise duties on energy, VAT on energy and on some taxes have already reduced inflation by about 2%.

It is actually even worse: the CPB predicts that 9.5% of the children in our rich country will live in poverty next year. This is also stated in the draft EIA, the document that outlines the economic environment after which the cabinet is finalising the budget for next year. It is difficult to see the CPB document in any other way than a 'call to action'.

This year, our economy is still growing by 4.6%. Two-thirds of this was already realised in the first half of the year. Next year, the growth will still be 1.1%, according to the CPB.

The skyrocketing fundamentals have eroded the purchasing power of households in recent years with extra savings and now that life is free again, there is plenty of spending despite extremely negative consumer confidence. In addition, all households are not already fixing the prices for a longer period of time due to the larger electricity bills.

The government has considerable financial scope to do something to restore purchasing power. Next year, if policy remains unchanged, the budget balance will be -1.1% of GDP (and the government debt at 47.1% of GDP). DNB warned this week against generic measures to compensate people for the loss of purchasing power. According to DNB, this will only make the inflation problems worse. After all, inflation is mainly caused by an imbalance between the supply and demand of goods and services in the economy. Large-scale generic purchasing power support will boost consumer demand and thereby exacerbate that supply-demand imbalance, exacerbating the inflation problem. There is not much that can be said about that per se. It is a bit wry that the institution that has long spectacularly underestimated and downplayed inflation now suddenly knows exactly what to do and how not to do it.

The government should also realise that this year households up to 120% of the social minimum were helped once with an energy subsidy of €1,300. If this is not repeated, there is a risk of a considerable loss of purchasing power for this group in 2023.

For the first time, the CPB has published figures on poverty. People live in poverty when their net income is less than able to meet their basic needs. This year 6.7% of the people in our country live in poverty, next year it will be 7.6%. This is even more unfavorable for children: 9.5% next year.

The demand is high, the causes are clear and the financial scope is available. I think that adds up to a decent package of measures on Budget Day. We shall see.

GDP growth explodes

The Dutch economy grew by 2.6% in the second quarter compared to the first quarter. That was much more than could reasonably be expected. Many details have not yet been published, but CBS reported that especially investment and foreign trade had generated a lot of growth. When asked, CBS acknowledged that the figures on investments were flattered by the delivery of ships and aircraft. Our growth was well above that in many other countries. Germany recorded a minuscule minus, Belgium +0.2% and the countries that benefited from the tourism revival grew slightly faster: about 1% for Italy and also Spain. The difference with Germany is getting bigger and bigger and is quite remarkable, as the following picture shows.

Source: Refinitiv Datastream

Source: Refinitiv Datastream

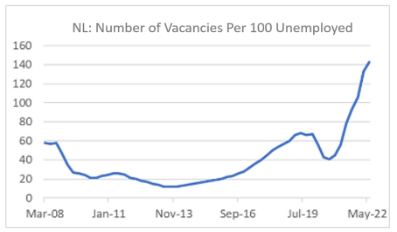

The unemployment rate in our country rose slightly for the third month in a row in July: 3.6% against 3.4% in June. The number of unemployment benefits fell slightly: -4,000 to 157,000. At the same time, CBS reports that the labor market tightened again in the second quarter. In the first quarter there were still 133 vacancies for every 100 unemployed, in the second quarter that number increased to 143 for every 100 unemployed. 38% of all entrepreneurs say that a shortage of staff is the main obstacle to their production or activities.

Source: Refinitiv Datastream

Total confusion in the US

Economic indicators in the US currently paint a very confusing picture. Clearly strong positive and negative indicators alternate. The housing market is quite sluggish. The National Association of Home Builders (NAHB) confidence index fell to 49 in August from 55 in July, marking the eighth monthly decline in a row. The NAHB speaks of a 'housing market recession'. This is caused by the increased mortgage interest and the increased construction costs. The fact that the latter factor is apparently starting to weigh heavily is evidenced by the fact that confidence continues to weaken, while mortgage rates have fallen slightly again in the past two months. The housing market therefore seems to have a little more empty than the interest rate. The number of existing homes sold fell again in July and was about 25% lower than in January.

Source: Refinitiv Datastream

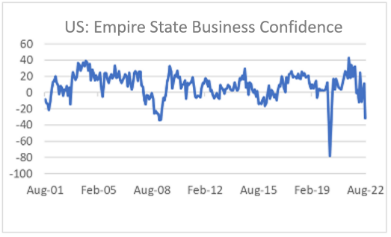

The Empire State index, which measures producer confidence in the Federal Reserve district of New York, fell sharply in August. In July, the index was still at 11.1 but in August it reached the fifth lowest level ever in the past 20 years: -31.3.

Source: Refinitiv Datastream

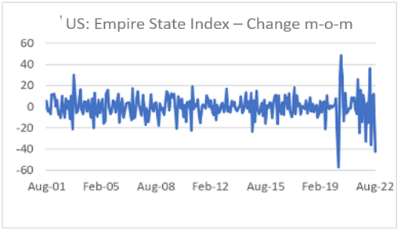

The decrease was therefore the third strongest one in a month. Only the decline in March and April of 2020 was greater. Now, this is a confidence index measured in a limited regional area, so we have to be careful with the interpretation. However, this is a remarkably strong decrease.

Source: Refinitiv Datastream

Against this negative, a comparable confidence indicator related to the Federal Reserve district of Philadelphia actually improved in August: +6.2 from -12.3 in July.

Also positive in the US is that the industry still manages to expand their production. Production in the manufacturing sector increased by 0.7% m-o-m in July, which is 3.2% higher than a year earlier. That's not overly strong but certainly not a recession, not even close.

The US labour market also appears to be stabilising. The number of applications for unemployment benefits was 250,000 in the week of August 13. The number of applications had increased in the second half of June and the first half of July, but that increase has now stopped.

I've had several discussions lately about whether or not the economy is going to go into recession. For Europe – and the Netherlands – that chance seems very high to me, especially because of the enormous loss of purchasing power. The US has a slightly better chance of getting out of hand. It should be noted that the yield curve in the US (i.e. the difference between the effective yield on 10-year and 2-year government bonds) has been negative for some time now. In the last 50 years, every US recession has been preceded by such an inverted interest rate structure.

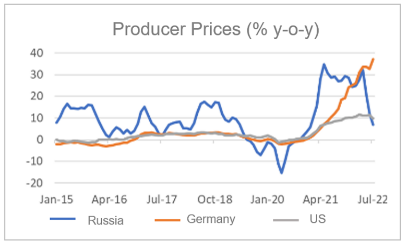

Is Russian inflation stabilising?

There is no doubt that the Russian economy is suffering greatly from the war and sanctions. The policymakers in Moscow are obviously trying to manage the economy in the best possible way. I don't know if we can believe the published numbers. But my eye fell on Russian producer prices this week. In the following chart I have compared it with those in Germany and the US. The German figures look very bad. Until the beginning of 2021, these ran strikingly parallel to the American one, but that picture has changed significantly. European gas prices will undoubtedly play a major role in this. Furthermore, it appears that the Russians seem to be doing a pretty good job of controlling producer-level inflation, which is often seen as a precursor to consumer-level inflation.

For what it's worth, of course.

Source: Refinitiv Datastream

In conclusion

It is inevitable that the government will come up with an extensive package of measures on Budget Day to support the purchasing power of the most vulnerable groups. Indicators about the American economy currently present a very diverse picture. While I continue to think that many countries will experience a period of real contraction between now and the end of next year, Americans have a better chance of avoiding the recession than we do.