Google Translated from Dutch to English. Link to the original post in Dutch below.

- Uncertainty about short-term economic developments is particularly high

- The CPB and the ECB seem much too optimistic to me,…

- …but the panic story of VNO-NCW also seems a bit exaggerated to me

- The US now has a huge inflation problem

Google Translated from Dutch to English. Here is the link to the original article in Dutch. The article was originally published on 11 March 2022

The current level of economic uncertainty is apparent from the noises that can be heard from various quarters. The CPB calculates that the loss of purchasing power will be 2.7% on average this year, but that purchasing power will increase again by 1.9% next year. The CPB also forecasts 3.7% economic growth for this year. Coincidentally, the ECB also forecasts 3.7% economic growth for the eurozone this year. That may sound unrealistic. However, it should be borne in mind that the so-called statistical overflow is already 2.7 percentage points. (GDP in the last quarter of 2021 was 2.7% higher than the average for the year, so even if GDP stays the same for the full year as the fourth quarter of 2021, growth of 2.7% will be on the books before 2022.)

Nevertheless, the growth forecasts of CPB and ECB seem unrealistic. They see the war as a temporary shock that we will soon overcome. The ECB does have two alternative scenarios, a worse and a much worse scenario, but remarkably enough, during Ms Lagarde's press conference on Thursday, the word recession was not mentioned.

Perhaps these optimistic sounds demanded a response. VNO-NCW foresees a prolonged recession and chairman Ingrid Thijssen gives the impression that the war has caused a sort of infarction in which a large number of deliveries have come to a standstill. I try diligently to inform myself. The chairman of VNO-NCW will not pull this off her thumb. A few entrepreneurs I spoke to recognise themselves much more in Thijssen's story than in that of the CPB and the ECB. The logistics chain is once again completely disrupted. Purchasing prices continue to rise and suppliers often do not even want to submit quotations. The problem, of course, is that we don't know how long this will take.

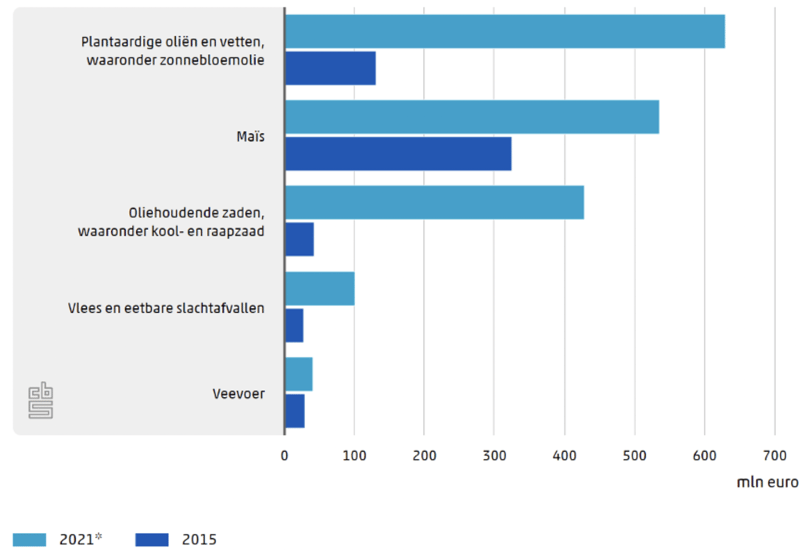

I too lean more towards the VNO-NCW story, but I still have doubts about that negative view. Statistics Netherlands recently published an article about our trade with Ukraine. Imports from that country have increased twelvefold in 20 years. That is a major achievement by the Ukrainian exporters. But the total amount was only slightly more than EUR 2 billion last year. And these are the main products:

Top 5 products with largest import value from Ukraine

If that all comes to a halt, that's annoying, but I don't think it's the start of a prolonged recession. Of course I understand that it is not just about the mutual trade relationship, but still… The economy of Ukraine in 2021 was slightly less than one sixth of the Dutch economy.

From Russia, we imported EUR 18.4 billion in 2021, of which 16.1 mineral fuels and a mere EUR 2.3 billion other products. We really can't do without those fuels and most of them will continue as usual for the time being. If the gas tap were to close, major problems could be foreseen.

The problem for institutions such as the CPB and the ECB is that they work with models and that recent major shocks, such as the war, are difficult to process quickly. My personal opinion is that the CPB and the ECB are probably too optimistic. On the other hand, the problem for an organisation such as VNO-NCW is that they are confronted with the emotion of the day. And I suspect that the forecast of a prolonged recession is too negative. It is clear that the uncertainties are enormous. Perhaps most clearly, the European gas price has fluctuated between EUR 75 and EUR 300 MWH over the past four weeks, while a price of EUR 15-20 MWH was normal for the pandemic.

The US has a giga-inflation problem

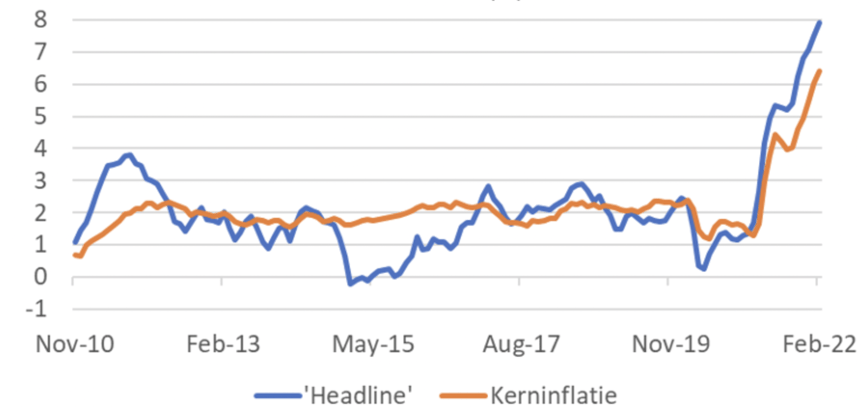

Inflation in the US rose further in February: 7.9% and excluding food and energy: 6.4%. Due to the further rise in oil prices, inflation will certainly not come down any time soon.

USA: Headline v Core Inflation (%)

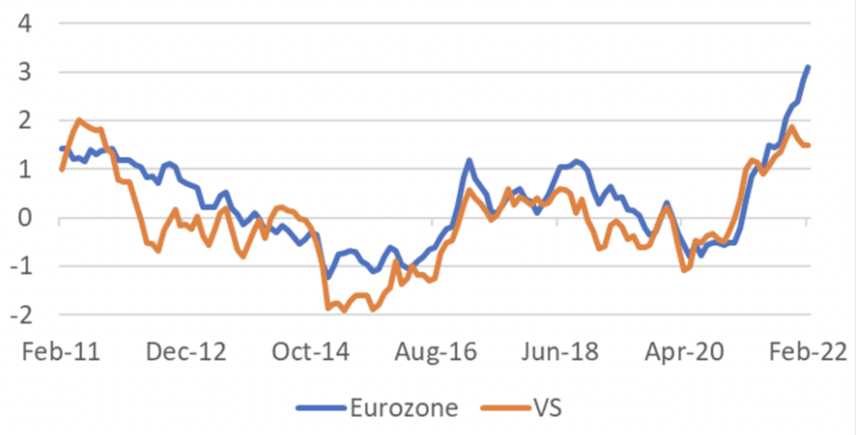

Inflation has also risen in Europe. Still, I think the problem is much bigger in the US than it is here. During the ECB press conference, Ms Lagarde reiterated that more than half of inflation in the eurozone is caused by energy prices. In the US, the inflation process is much broader. The following picture shows the difference between headline inflation, also known as the headline, and core inflation (that is, for the US excluding food and energy and for the eurozone excluding food, energy, alcohol and tobacco). I would like to draw your attention to the most recent development. The difference between the two measures of inflation is much greater in the eurozone than in the US. This confirms that inflation in the US is broader in nature than in the eurozone.

Eurozone / USA: Headline minus Core Inflation (%)

I told you so

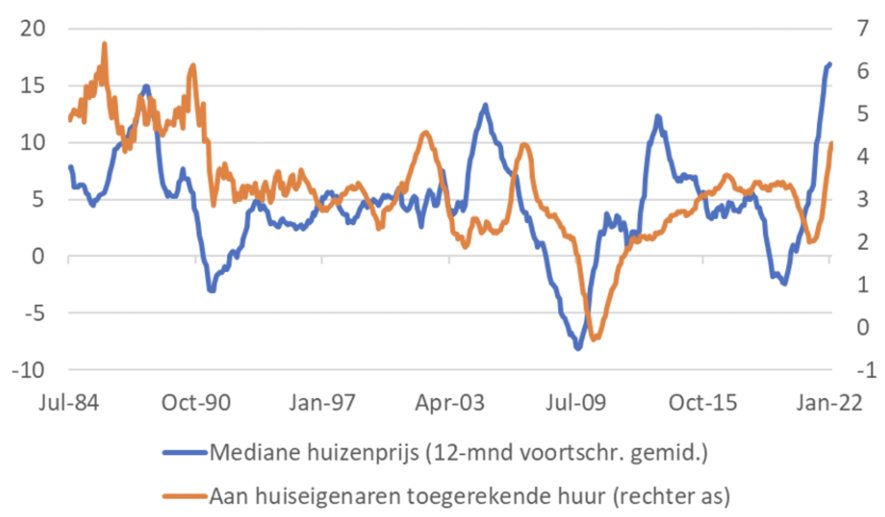

A huge problem for the US is the housing market. House prices have risen sharply. Rents in the US follow house prices, albeit with some delay. Rents of houses that are actually let have a weight of 7.4% in the US inflation basket. Rents imputed to homeowners even have a weight of 24.2%. Rising house prices are therefore tapping into the inflation figure with some delay. I have written about this regularly. The following chart shows that imputed rents are now 4.3% higher than a year ago. Figures from Zillow (say the US Funda) on rents suggest that the increase is accelerating rather than slowing down. When energy prices stop rising, the total inflation rate can never reach 2% quickly. I suspect US inflation will remain above 4% for a long time.

USA: House Prices & Rent (% y-o-y)

In contrast to Europe, wage growth in the US has already picked up strongly. An interesting indicator for this is compiled by the Federal Reserve of Atlanta, the 'median wage growth tracker'. As the following picture shows, the median wage growth has since accelerated to 5.8%, the largest increase ever, ie in the 25 years that these numbers have been tracked. If you assume that productivity in the US will rise on a 1-1.5% trend, it is difficult to see how inflation could fall below 4% in the foreseeable future, given this wage increase.

USA: Atlanta Fed "Media Wage Growth Tracker"

For the time being, wage growth in our part of the world appears to be much more limited than in the US. That's why I think the inflation problem in the US is much bigger than it is with us. But it may be that the acceleration of wage growth in Europe is already underway but has yet to show up in the statistics. Incidentally, the labour market in the Netherlands is much tighter than in other euro countries.

Powell will speak next week

The Federal Reserve's Policy Committee will meet next week. It is inevitable that they will raise interest rates. We are curious what they will say about the impact of the war on the economy, on the financial markets and therefore on the outlook for monetary policy. Although the influence of the war on the US economy is less pronounced than on our own, I think that the Fed will also initially underestimate its influence. Ultimately, I suspect they will moderate the pace of rate hikes somewhat over the course of the year.

Closing

The economic outlook is very uncertain. The forecasts of the CPB and the ECB seem unrealistically optimistic to me. In the eurozone, some economic contraction seems inevitable to me. It is only logical that the uncertainty has shaken confidence among companies. And it seems logical to me that the logistics chain has been disrupted again. Still, I think the prospect that VNO-NCW outlines, a prolonged recession, is a bit exaggerated. The Russian and Ukrainian economies are not big and important enough for that.

Inflation in the US is now 7.9%. The Fed has made a huge error of judgment here. Even if a decline eventually sets in, I estimate that US inflation will remain above 4% for a long time. Although the Fed may make slightly fewer rate hikes this year in connection with the war than it would have done without the war, the US official interest rate should eventually rise quite sharply.