- Dutch unemployment is rising... now partly due to a decrease in the number of jobs

- US and Europe economy diverges

- Better numbers from China

- Disappointing inflation in the US puts stock markets under pressure

- Fed will raise interest rates even further.

Google Translated from Dutch to English. Here is the link to the original article in Dutch. The article was originally published on 16 September 2022.

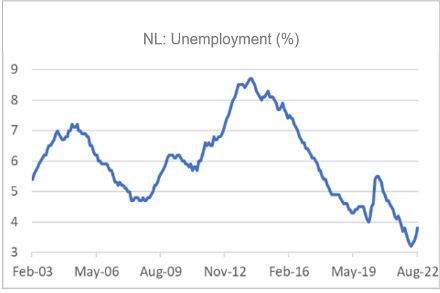

Unemployment in our country rose again in August: 3.8%, against 3.6% in July and a lowest level of 3.2% in April. The graph shows that unemployment is historically still very low. It should be noted that the rise in unemployment from April to July was entirely due to an increase in the number of people entering the labour market. The number of workers continued to increase in those months. August saw the first decline in total employment. At least, on the basis as CBS looks at it: the number of employed people decreased by an average of 3,000 per month in the three (3) months to August.

Source: Refinitiv Datastream

In my view, how this will continue depends mainly on the gas price. It determines to a large extent whether we end up in a recession or not and how deep it will be. I am an optimistic person, but find it difficult to be very optimistic about this. The ECB only foresees a recession for the eurozone in a 'risk scenario'. The economists at most Dutch banks do predict a recession for our country, but then immediately add the qualification mildly. Okay, companies and households have relatively healthy balance sheets, so there is no need for a balance sheet recovery that will cause a recession. Perhaps that will keep the recession mild. On the other hand, the policy room to stimulate is much more limited than in many previous recessions. But above all: the erosion of the purchasing power of households is unprecedented, as is the increase in the energy costs of companies. Maybe I can wake you up with some numbers.

In 1973 and 1974, the oil price rose by about 375%. It was enough to trigger a global, nasty recession. At the time of writing (€225 MWh) the European gas price is 1500% (yes, fifteen hundred, no typo) higher than before the pandemic. Now gas plays a different and perhaps lesser role in our economy than oil did back then, but this is a price shock that, in Europe at least, is four times greater than that of oil in 1973/74. According to figures from the International Energy Agency, gas provided 45% of the total primary energy needs in our country in 2020 (wind and solar combined 3.2%) and about 60% of electricity production (wind 12%, solar 7% ). By way of comparison, gas provided 27% of the total German primary energy requirement in 2020 (wind and solar combined 6%) and 17% of the electricity production (wind 22%, solar 9%). We use more gas than most other neighbouring countries and we are therefore more affected by the sharp rise in gas prices.

Only if the gas price falls sharply can we avoid a recession 'in my humble opinion'. Perhaps the advance of the Ukrainian army offers hope.

Divergence European and American economy

In the meantime, signs are emerging that the economic situation in the US and the eurozone is each choosing its own path. This means that the US economy is developing more strongly than the European one. This is not surprising, because the rise in energy prices in the US is much smaller than ours and the war zone is much further away, making it less disruptive.

For example, manufacturing production in the US was 3.3% higher in August than a year earlier (July +2.9%) while production in the eurozone in July (latest figure) was 2.6% lower than in July. a year earlier.

Source: Refinitiv Datastream

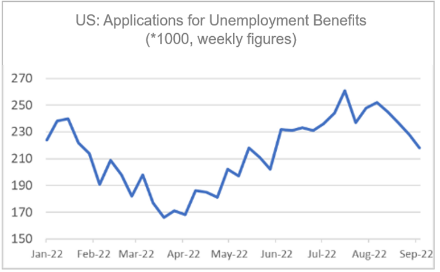

And while it appears that our labour market is taking a turn with rising unemployment rates, the US labour market remains robust. From April, the number of applications for unemployment benefits rose slightly every week, but has been declining again for two (2) months.

Slightly better news from China

We should certainly not celebrate too soon and the Chinese real estate sector seems 'an accident waiting to happen', but the Chinese economy is recovering as restrictions on public life are easing. In August, manufacturing production was 4.2% higher than a year earlier (July 3.8%), better than expected. The increase in automotive production accelerated from 22.5% to 30.5%. Perhaps that is not only a sign of China's recovery but also a reduction in chip shortages in the sector worldwide.

Retail sales growth also accelerated more than expected in August: +5.4% yoy, from +2.7% in July. If the lockdowns ease, the 'shoppers' will apparently show themselves again immediately.

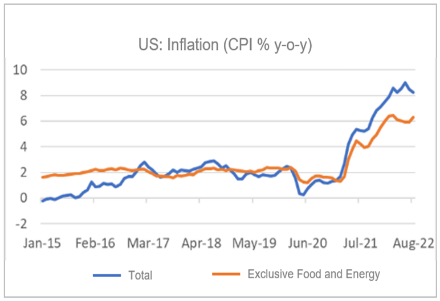

US inflation disappointed in August

Equity markets, especially the US, took a hit this week immediately after the release of US inflation data for August. This was because 'core inflation' (ie inflation figures excluding food and energy) was rather disappointing. Prices excluding food and energy rose 0.6% from July and 6.3% from August 2021; in July the year-on-year figure was still 5.9%. This setback fueled the idea that the Fed will not hesitate to decide on another 0.75% rate hike next week and then hike rates even further. The stock markets therefore struggled with this.

Total inflation was only 0.1% m-o-m, but that was also a bit disappointing because the oil prices, and thus the petrol prices, the prices for heating oil, etc. had fallen quite sharply. The headline inflation rate in the US now stands at 8.3%, after 8.5% in July. We are jealous of it.

Source: Refinitiv Datastream

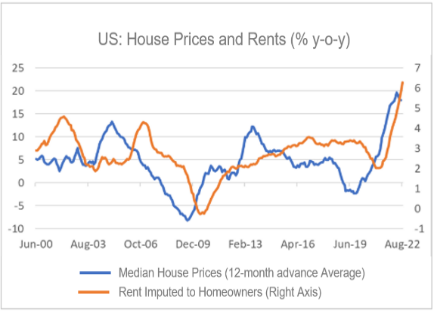

Three things are important: renting, renting and renting

In the past, I have frequently pointed out the importance of "rents" in US inflation figures. Actual rents and rents imputed to homeowners have a weight of 30.9% in the US inflation basket (approximately 23%). In the basket of core inflation, it is even close to 40%. In the US, rent increases are following house prices quite well, albeit with a certain lag, as can be seen in the following chart.

Source: Refinitiv Datastream

A year ago, rents were still rising at a rate of more than 2% per year. In August, however, they were about 6.5% higher than a year ago. In the meantime, the rate of increase in house prices is slowing down. Now that the capital market interest rate, and with it the mortgage interest rate, has risen again, the housing market will cool down further. A reduction in rent increases can therefore be expected and with it a moderation of inflation. Only…..in view of the delays, that can take quite a while.

On balance, I think that US inflation is going to drop soon anyway. The road to 2% is a long one, but it may go faster in the course of 2023 than currently expected. There are a few reasons for that:

- The international economy is weakening and so is the American economy.

- The rise in house prices is already moderating, may turn into price falls and that will put pressure on rents.

- The rise in producer prices is already clearly moderating, following the fall in the price of many raw materials.

- The costs of companies continue to fall due to the now sharp fall in sea freight costs.

- Consumer inflation expectations, as estimated by participants in financial markets, are falling.

- Wage growth is currently stabilising. According to the (weighted) Atlanta Fed wage growth tracker, the rate of wage growth has fallen fractionally over the past two (2) months.

None of this will stop the Fed from raising official interest rates quite a bit, starting in the coming week. They simply take the risk that they thereby contribute to the emergence of a recession because they consider a recession less harmful to the economy in the longer term than high inflation.

Closing

I'm an optimistic economist, but now, I'm struggling. Maybe I should go on antidepressants or go to a coffee shop now and then…. I have often discussed the insane European gas price. In my opinion, the impact this will have on our economy cannot be overestimated. If the price of gas does not fall significantly soon, a recession seems inevitable to me and why it should remain "mild" or "light", as many banking economists are currently claiming, is not entirely clear to me.

Now that China has put the many lockdowns behind it, things are going a bit better there, but that economy still has plenty of challenges and the lockdowns could come back again.

The US economy is stronger than ours, but the Fed looks set to get inflation under control as soon as possible. If you raise interest rates enough, you will certainly succeed, albeit at the expense of a recession.